asdf

asdf

Notes: All subscriber numbers in thousands. For LEC ISPs, subscriber numbers generally do not include affiliated video subscription to satellite video programming. Data obtained from 2010-2015 SEC Annual Reports (10-K) for each firm.

Casual observation of Table 1 shows that the number of Internet subscribers has continued to grow between 2010 and 2015 for most ISPs, whether cable or LEC. In contrast, casual observation of Table 2 shows that the number of video subscribers has declined for most cable companies, but grown for most LECs over this time-frame, though LEC video subscribership remained substantially below that of the cable companies.

The general trend in Table 1 will not be surprising to Internet researchers or people who have not been living under a rock. The Internet has been kind of a big deal the last few years. For example, it has fostered business innovation (Brynjolfsson and Saunders 2010; Cusumano and Goeldi 2013; Evans and Schmalensee 2016; Parker, Van Alstyne, and Choudary 2016), economic growth (Czernich et al. 2011; Greenstein and McDevitt 2009, Kolko 2012), my ability to blog, and your ability to consume the items in the hyperlinks above.

The trends in Table 2 are less well known outside the world of Internet research and business practice and are at least in part attributable to historical developments involving the Internet. As described by Greg Rosston (2009), LECs initially got into the business of high-speed broadband to improve upon their previously offered dial-up Internet services—they were not initially in the multichannel video programming distribution (MVPD) market. In contrast, the cable companies became ISPs after it became apparent that coaxial cables used to transmit cable television signals could also be used for high-speed broadband.

Thus, whereas cable companies could use their networks to offer subscribers video and Internet bundles, many LECs have had to partner with satellite video programming distributors or resell competitors’ services to be able to advertise a bundled service. Eventually, some LECs acquired their own video customers either through purchases of smaller cable competitors in certain areas, or by relying on Internet Protocol television (IPTV), either through construction of fiber networks that deliver service to the home as was the case with Verizon or by doing whatever it is that AT&T does. This has explained the growth of LEC video customers, whereas competition from LECs, video on demand, and mobile wireless service providers should at least partly explain the decline in cable video subscribership.

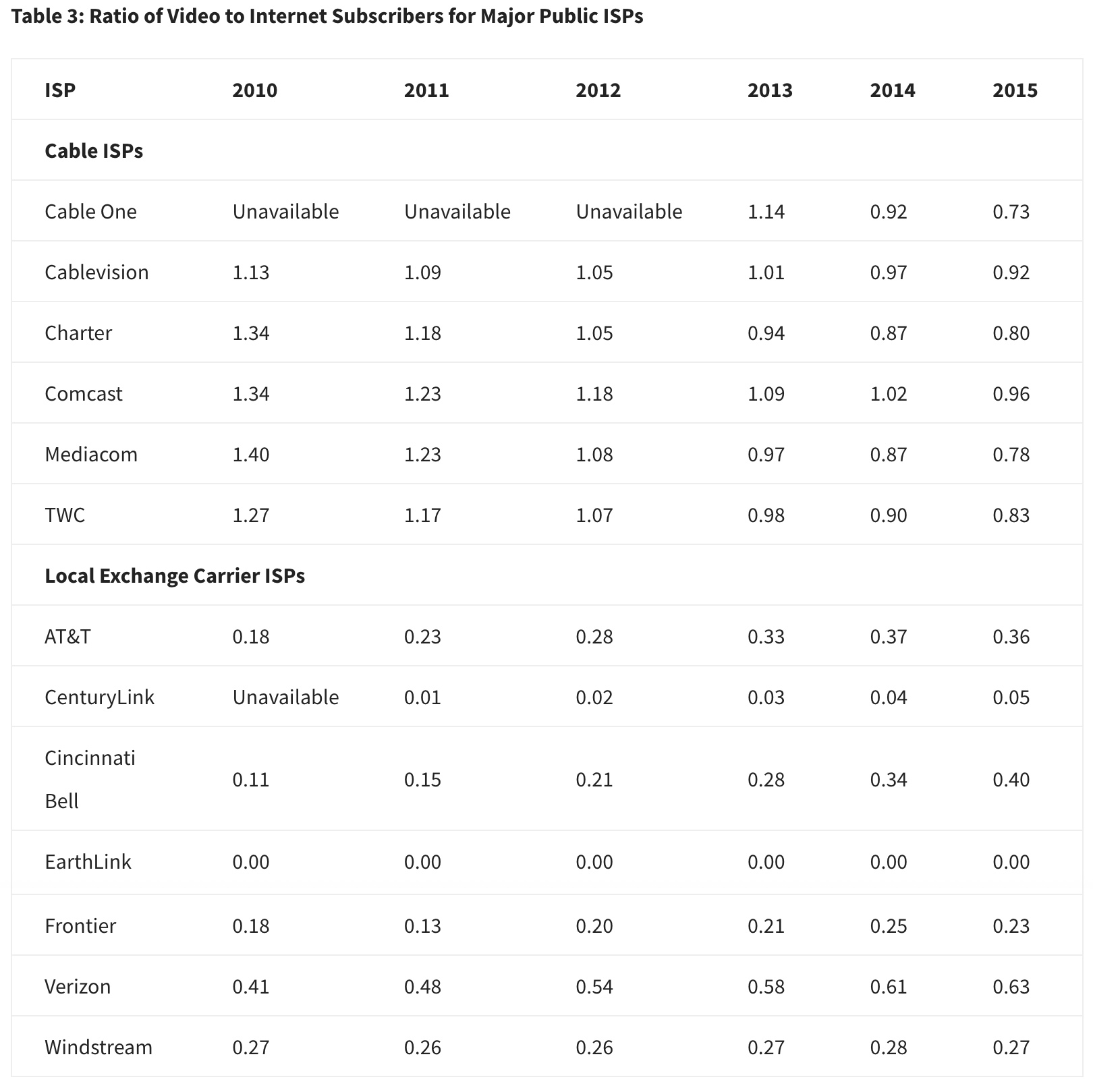

To put these trends into perspective, I have included one additional Table (Table 3), which displays the ratios of video to Internet subscribers for the ISPs above. As the Table makes evident, the ratios have declined for most cable companies and increased for most LECs between 2010 and 2015. If I had to make an educated guess, the cable company trend will continue in the coming years, but I am less certain that the trend on the LEC side is sustainable as video on demand and mobile wireless continue to eat into the traditional video market.

Notes: Ratios represent the fraction of residential and non-enterprise business customers who subscribe to a video service relative to those who subscribe to high-speed Internet. For LEC ISPs, ratios generally do not include affiliated video subscription to satellite video programming.

If you want to reuse or make fancy graphs out of the data located in this post, please attribute the data to Aleksandr Yankelevich, Quello Center, Michigan State University.