So what is the Commission to do prior to the transition? According to the Senate Committee on Commerce, Science, and Transportation, the FCC can “focus its energies” on “many consensus and administrative matters.” Presumably, this includes the FCC’s ongoing incentive auction, now set for its fourth round of bidding, and subject to its own controversies, with dissenting votes on major items released in 2014 (auction rules and policies regarding mobile spectrum) by Republican Commissioners concerned about FCC bidding restrictions and “market manipulation,” along with a statement by a Democratic Commissioner saying that FCC bidding restrictions did not go far enough.

The Incentive Auction

Initially described in the 2010 National Broadband Plan, the Incentive Auction is one of the ways in which the FCC is attempting to meet modern day demands for video and broadband services. The FCC describes the auction for a broad audience in some detail here and here. In short, the auction was intended to repurpose up to 126 megahertz of TV band spectrum, primarily in the 600 MHz band, for “flexible use” such as that relied on by mobile wireless providers to offer wireless broadband. The auction consists of two separate but interdependent auctions—a reverse auction used to determine the price at which broadcasters will voluntarily relinquish their spectrum usage rights and a forward auction used to determine the price companies are willing to pay for the flexible use wireless licenses.

Repackaging

What makes this auction particularly complicated is a “repackaging” process that connects the reverse and forward auction. The current licenses held by broadcast television stations are not necessarily suitable for the type of contiguous blocks of spectrum that are necessary to set up and expand regional or nationwide mobile wireless networks. As such, repackaging involves reorganizing and assigning channels to the remaining broadcast television stations—that remain operational post-auction—in order to clear spectrum for flexible use.

The economics and technical complexities underlying this auction are well described in a recent working paper entitled “Ownership Concentration and Strategic Supply Reduction,” by Ulrich Doraszelski, Katja Seim, Michael Sinkinson, and Peichun Wang (henceforth Doraszelski et al. 2016) now making its way through major economic conferences (Searle, AEA). As the authors point out with regard to the repackaging process (p. 6):

[It] is visually similar to defragmenting a hard drive on a personal computer. However, it is far more complex because many pairs of TV stations cannot be located on adjacent channels, even across markets, without causing unacceptable levels of interference. As a result, the repackaging process is global in nature in that it ties together all local media markets.

With regard to the reverse auction, Doraszelski et al. (2016) note that (p. 7):

[T]he auction uses a descending clock to determine the cost of acquiring a set of licenses that would allow the repacking process to meet the clearing target. There are many different feasible sets of licenses that could be surrendered to meet a particular clearing target given the complex interference patterns between stations; the reverse auction is intended to identify the low-cost set . . . if any remaining license can no longer be repacked, the price it sees is “frozen” and it is provisionally winning, in that the FCC will accept its bid to surrender its license.

The idea is that the FCC should minimize the total cost of licenses sold on the reverse auction while making sure that its nationwide clearing target is satisfied. As Doraszelski et al. (2016) note, the incentive auction has various desirable properties. Of particular note is strategy proofness (see Milgrom and Segal 2015), whereby it is (weakly) optimal for broadcast license owners to truthfully reveal each station’s value as a going concern in the event that TV licenses are separately owned.

Strategic Supply Reduction

However, the author’s main concern in their working paper is that in spite of strategy proofness, the auction rules do not prevent firms that own multiple broadcast TV licenses from potentially engaging in strategic supply reduction. As Doraszelski et al. (2016) show, this can lead to some fairly controversial consequences in the reverse auction that might compound any issues that could arise (e.g., decreased revenue) due to bidding restrictions in the forward auction. Specifically, the authors find that multi-license holders are able to earn large rents from a supply reduction strategy where they strategically withhold some of their licenses from the auction to drive up the closing price for the remaining licenses they own.

The incentive auction aside, strategic supply reduction is a fairly common phenomenon in standard economic models of competition. Consider for instance a typical model of differentiated product competition (or the Cournot model of homogenous product competition). In each of these frameworks, firms’ best response strategies lead them to set prices or quantities such that the quantity sold is below the “perfectly competitive” level and prices are above marginal cost—thus, firms individually find it optimal to keep quantity low to make themselves (and consequently, their competitors) better off than under perfect competition.

In the incentive auction, a multi-license holder that withdraws a license from the auction could similarly increase the price for the remaining broadcast TV licenses that it owns (as well as the price of other broadcast TV license owners). However, in contrast to the aforementioned economic models, in which firms effectively reduce supply by underproducing, a firm engaging in strategic supply reduction is left with a TV station that it might have otherwise sold in the auction. The firm is OK with this if the gain from raising the closing price for other stations exceeds the loss from continuing to own a TV station instead of selling it into the auction.

Example 1

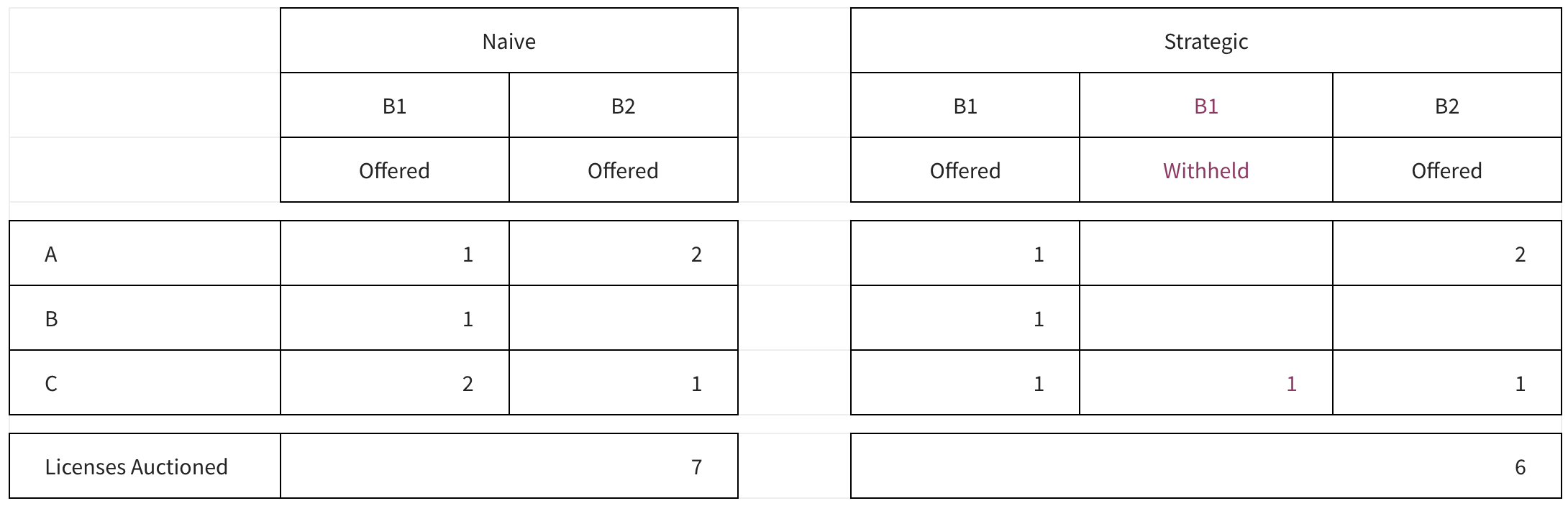

Consider the following highly stylized example of strategic supply reduction: There are two broadcasters, B1 and B2, in a market where the FCC needs to clear three stations (the reverse auction clearing target) and there are three different license “qualities,” A, B, and C, for which broadcasters have different reservation prices and holdings as follows:

Suppose that the auctioneer does not distinguish between differences in licenses (this is a tremendous simplification relative to the real world). Consider a reverse descending clock auction in which the auctioneer lowers its price in decrements of $2 starting at $10 (so $10 at time 1, $8 at time 2, and so on until the auction ends), and ceases to lower its price as soon as it realizes that any additional licensee drop outs would not permit it to clear its desired number of stations (as would for instance happen when quality A and B licenses drop out). Suppose that a broadcaster playing “truthfully” that is indifferent between selling its quality license and dropping out remains in the auction (so that for instance, A quality licenses are not withdrawn until the price falls from $10 to $8).

In a reverse descending clock auction in which broadcasters play “naïve” strategies, each broadcaster would offer all of their licenses and drop some from consideration as the price decreases over time. However, there is another “strategic” option, in which B1 withholds a quality C license from the auction (B1 can do so by either overstating its reservation price for this license—say claiming that it is $10—or by not including it in the auction to begin with):

The results of the naïve bidding versus the strategic bidding auction are quite different. In the naïve bidding auction, the auctioneer can continue to lower its price down to $4 at which point B1 pulls out its B quality license and the auction is frozen (further drop outs would not permit the desired number of licenses to be cleared). Each broadcaster earns $4 for each quality C license with B1 earning a profit of 2×($4-$2)=$4.

Suppose instead that broadcaster B1 withheld one quality C license. Then the auction would stop at $8 (because there are only three licenses left as soon as A quality licenses are withdrawn). Each broadcaster now earns $8 per license sold, with B1 earning a profit of ($8-$6)+($8-$2)=$8. Moreover, B2 benefits from B1’s withholding, earning profit of $6 instead of $2, as in the naïve bidding case. The astute reader will notice that B1 could have done even better by withholding its B quality license instead! This is a result of our assumption that the auctioneer treats all cleared licenses equally, which is not true in the actual incentive auction. Finally, notice that even though B2 owns three licenses in this example, strategic withholding could not have helped it more than B1’s strategic withholding did unless it colluded with B1 (this entails B2 to withhold its quality A licenses and B1 to withhold both quality C licenses).

Evidence of Strategic Supply Reduction

Doraszelski et al. (2016) explain that certain types of geographic markets and broadcast licenses are more suitable for strategic supply reduction. They write:

First, ideal markets from a supply reduction perspective are [those] in which the FCC intends to acquire a positive number of broadcast licenses and that have relatively steep supply curves around the expected demand level. This maximizes the impact of withholding a license from the auction on the closing price . . . Second, suitable groups of licenses consist of sets of relatively low value licenses, some with higher broadcast volume to sell into the auction and some with lower broadcast volume to withhold.

What is perhaps disconcerting is the fact that Doraszelski et al. (2016) have found evidence indicating that certain private equity firms spent millions acquiring TV licenses primarily from failing or insolvent stations in distress, often covering the same market and in most instances on the peripheries of major markets along the U.S. coasts. Consistent with their model, the authors found that many of the stations acquired had high broadcast volume and low valuations.

Upon performing more in depth analysis that attempts to simulate the reverse auction using ownership data on the universe of broadcast TV stations together with FCC data files related to repacking—the rather interesting details of which we would encourage our audience to read— Doraszelski et al. (2016) conclude that strategic supply reduction is highly profitable. In particular, using fairly conservative tractability assumptions, the authors found that simulated total payouts increased from $17 billion under naïve bidding to $20.7 billion with strategic supply reduction, with much of that gain occurring in markets in which private equity firms were active.

Example 2

Suppose that in our example above that the quality C stations held by broadcaster B1 were initially under the control of two separate entities, call these B3 and B4. Then, if B1, B2, B3, and B4 were to participate in the auction, strategic withholding on the part of B1 would no longer benefit it. However, B1 could make itself better off by purchasing one, or potentially both of the individual C quality licenses held by B3 and B4. Consider the scenario where B1 offers to buy B3’s license. B3 is willing to sell at $4 or more, the amount it will earn under naïve bidding in the auction and Bertrand style competition between B3 and B4 will keep B1 from offering more than that. With a single C quality license, B1 can proceed to withhold either its B or C quality license, raise the price to $8, and benefit both itself, and the other broadcasters who make a sale in the auction.

This result, whether realized by the FCC ex-ante or not, is problematic for several reasons. First, it raises the prospect that revenues raised in the forward auction will not be sufficient to meet payout requirements in the reverse auction. As is, this has already occurred three times, with the FCC having had lowered its clearance target to 84 megahertz from the initial 126 megahertz; though we caution that the FCC is currently not permitted to release data regarding the prices at which different broadcasters drop out of the auction, so we cannot verify whether final prices in earlier stages of the reverse auction were impacted by strategic supply reduction. Second, as is the case with standard oligopoly models, strategic supply reduction is beneficial for sellers, but not so for buyers or consumers.

Third, strategic supply reduction by private equity firms raises questions about the proper role and regulation of such firms. The existence of such firms is generally justified by their role in providing liquidity to asset markets. However, strategic supply reduction seems to contradict this role, particularly so if withheld stations are not put to good use—something Doraszelski et al. (2016) don’t deliberate on. Moreover, strategic supply reduction relies on what antitrust agencies often term as unilateral effects—that is, supply reduction is individually optimal and does not rely on explicit or tacit collusion. However, whereas antitrust laws are intended to deal with cases of monopolization and collusion, it does not seem to us that they can easily mitigate strategic supply reduction.

Doraszelski et al. (2016) propose a partial remedy that does not rely on the antitrust laws: require multi-license owners to withdraw licenses in order of broadcast volume from highest to lowest. Their simulations show that this leads to a substantial reduction in payouts from strategic bidding (and a glance at Example 1 suggests that it would be effective in preventing strategic supply reduction there as well). Although this suggestion has unfortunately come too late for the FCC’s Incentive Auction we hope (as surely do the authors) that it will inform future auctions abroad hoping to learn from the U.S. experience.

This post was written in collaboration with Emily Schaal, a student at The College of William and Mary who is pursuing work in mathematics and economics. Emily and I previously worked together at the Federal Communications Commission, where she provided invaluable assistance to a team of wireless economists.